The Changing Landscape of Printing in 2019

The following article was originally published by Printing Impressions. To read more of their content, subscribe to their newsletter, Today on PIWorld.

In terms of overall business conditions, expect 2019 to look a lot like 2018 for the printing industry. Sales (all sources) will grow 1.5%-2.5%, to $87 billion, after growing roughly 1.7% this year, according to SGIA. And the intense pressure on margins will continue — created again by tight paper markets, tight labor markets, excess capacity and rising tariffs.

But there’s a lot more to commercial printing’s story than overall business conditions. There’s also ongoing change in what a commercial printer is and does — structural labor shortages; print’s changing role in communication; personalization, integration and interactive/mobile; and the realities of diversification.

Industry Convergence Trend Confirmed

A recent survey of the SGIA Commercial Printing Panel fills in the details. We first asked the panel to describe their companies. Responses show how extensively roles are changing. For example, more than 47% now describe themselves as a combination of company types rather than a single company type.

Descriptions include provider of mailing services (42.6%), provider of fulfillment services (28.2%) and provider of marketing services (20.1%). And while 72.7% include “general commercial printer” in their description, just 34% define themselves exclusively as a general commercial printer.

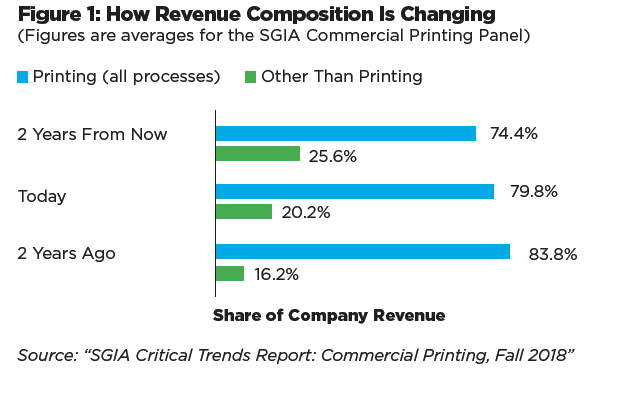

A discussion of revenue composition reinforces three critical points. First, the trend is clearly toward print, with our research group expecting something other than printing to provide, on average, 25.6% of their revenue by 2020, up from 20.2% today and 16.2% two years ago. (See Figure 1)

Second, not everyone is diversifying. Slightly more than one-fifth still get at least 90% of revenue from print and don’t expect that to change. More than a few are making it work.

Click to enlarge.

And, third, there’s big change within print. The panel projects revenue increases over the next two years, averaging 9.4% for wide-format, 5.6% for variable-content toner digital, 4.1% for inkjet and decreases averaging 1.1% for lithography.

We asked how client needs are changing. We learned that there is growing demand for faster turn times and shorter, more targeted runs; a broader range of services; advanced designs and special finishing to create distinctive print — the “wow factor” as one member of our panel puts it; and help maximizing the return on their communications dollar. That means:

- More moving parts. It isn’t just getting faster on a vanilla job. It’s quickly pulling together services, from database management to the design of standout direct mail, to the creation of multi-media communications programs.

- Minimizing the friction all those moving parts created by automating and smoothing workflows. “The more integration front to back, the more efficient we become” — minimizing steps and touches, eliminating processes that no longer add value, and the more efficient purchase and inventory of essential materials and supplies.

- Showing clients exactly how much value we create for them because they want more and faster, but aren’t always willing to pay for it.

- Pricing services added, whether individually or as part of a marketing/communications package, for competitiveness and profitability.

- Deciding how much to do inside and how much outside. Inside means more control and “one-stop shopping that simplifies the buying experience for clients.” Outside (with the right partner) means access to experience and expertise we don’t have and may not easily develop.

Click to enlarge.

Concerning labor shortages, the challenge for commercial printing goes beyond the cyclical — a 49-year low unemployment rate — to the structural — an old-economy image that makes it difficult to attract young personnel. The Print and Graphics Scholarship Foundation (PGSF) is one of the organizations working to correct that image. Every company that prints should be familiar with its “Graphic Communications as a Career,” “Adventures in Print: Choose Your Career in Graphic Communications,” and other resources.

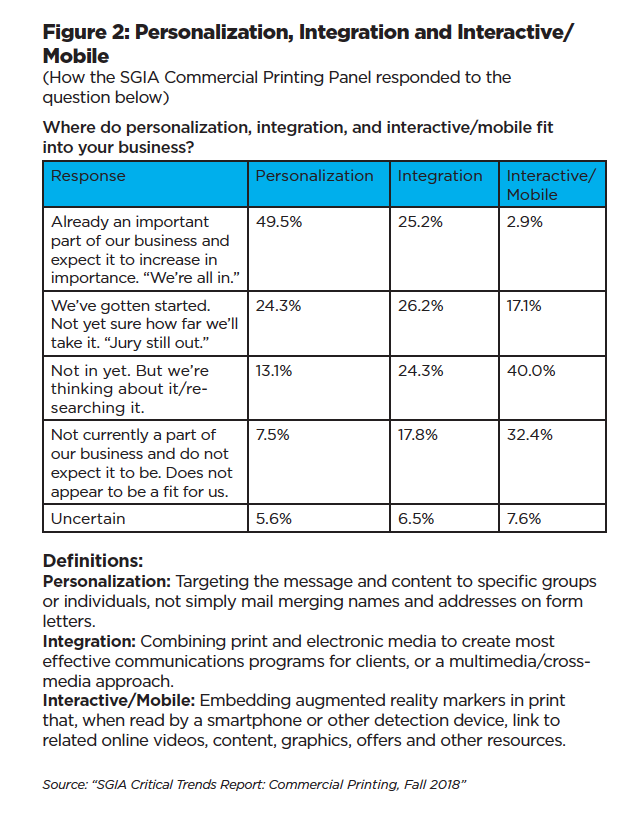

And then there’s what the “SGIA Critical Trends Report: Commercial Printing” describes as “thinking big and thinking carefully.” The big part is thinking beyond how print is manufactured to how print powers communication — particularly personalized, integrated, interactive/mobile communication. We asked our research panel where, if at all, the three fit in their plans. Among the responses, summarized in Figure 2:

- Personalization. Nearly half (49.5%) are all in and nearly one-quarter (24.3%) have gotten started, but aren’t sure how far they will take it. The difficulty of managing and securing complex databases and ensuring accurate personalization are obstacles for many.

- Integration. More than 50% are either all in (25.2%) or have gotten started (26.2%). But integration hasn’t won everyone over: 24.3% are thinking about it and 17.8% plan to stay focused on printing.

- Interactive/mobile. Only 17.1% have gotten started, while 32.4% do not include interactive/mobile in their plans.

Thinking carefully pertains to all diversification. It means we don’t rush in — no matter how much buzz that hot, new service is creating — but instead ask and honestly answer the following questions:

- How important is the service to our clients and prospects? Is it a must-have or nice but not essential? Can we prove it is a must-have?

- What’s really necessary to offer the service profitably?

- How will we market, sell and price the service?

- Do we have the personnel to offer it profitably? If not, where do we get them?

- Do we try it on our own? Or do we partner with an expert until we get to critical mass and high enough on the learning curve?

By taking those questions on, we greatly reduce the likelihood of missing an opportunity or of chasing something that, given our resources, capabilities and goals, will never be an opportunity.

We closed our survey by asking about the future. One Commercial Printing Panel member captured the thoughts of many when he described the future this way: “Our industry continues to evolve and it is not just a print business anymore. It is about communications and how we can best help clients communicate their message. If we help them get noticed we help them get business — that is what they are really paying us for!”

Productivity-enhancing, market-expanding technology will be necessary to achieve that future but not sufficient. We’ll also need advanced leadership and management skills. Companies that cultivate those skills will be the big winners. The more that do that, the more promising the commercial printing industry’s prospects in 2019 and beyond.

Andrew D. Paparozzi joined PRINTING United Alliance as Chief Economist in 2018. He analyzes and reports on economic, technological, social and demographic trends that will define the printing industry’s future. His most important responsibility, however, is being an observer of the industry by listening to the issues and concerns of company owners, executives and managers. Previously, he worked 31 years at the National Association for Printing Leadership. He has also taught mathematics, statistics and economics at various colleges. Andrew holds a Bachelor’s degree in economics from Boston College and a Master’s degree in economics — with concentrations in econometrics and public finance — from Columbia University.

Enfocus Presents ‘A Printing Carol’ Video

Enfocus Presents ‘A Printing Carol’ Video

Exploring HP's Wide-Format Strategy

Exploring HP's Wide-Format Strategy

Konica Minolta Announces Partnership with Taktiful

Konica Minolta Announces Partnership with Taktiful

Print Outlook: What to Expect in the Coming Year

Print Outlook: What to Expect in the Coming Year

Canon Hosts Stony Brook University Students for Job Shadow Day

Canon Hosts Stony Brook University Students for Job Shadow Day

The Crucial Role of Color Automation in Maintaining Brand Reputation

The Crucial Role of Color Automation in Maintaining Brand Reputation