Quad to Buy LSC Communications, Creating $8.1 billion Print Firm

The following article was originally published by Printing Impressions. To read more of their content, subscribe to their newsletter, Today on PIWorld.

Quad/Graphics Chairman Joel Quadracci is at the center of the printing industry universe following this week's blockbuster M&A deal.

It's not very often that the printing industry makes headlines among the top financial and business news of the day. But stuck somewhere below the seemingly endless drivel of pundit analysis concerning the pros and cons of Facebook's latest quarterly earnings report was the truly blockbuster news that Sussex, Wis.-based Quad/Graphics is acquiring LSC Communications, of Chicago. It will create a combined $8.1 billion, publicly-held company as the result of a whopping $1.4 billion all-stock transaction, which includes the refinancing of LSC Communications' debt.

Assuming regulatory approval, and following the approval of both Quad and LSC shareholders, the deal is expected to close in mid-2019. Quad/Graphics has secured a financing commitment from JPMorgan Chase Bank N.A. to refinance Quad’s existing credit facility and LSC Communications’ outstanding debt.

Annualized net synergies of the acquisition are expected to be approximately $135 million following the deal closing, and Quad/Graphics indicated those savings will be achieved in less than two years through the elimination of duplicative functions, capacity rationalization, improved operational efficiencies and greater efficiencies in supply chain management.

“This is a defining moment in Quad’s 47-year journey,” said Joel Quadracci, Quad/Graphics chairman, president and CEO. “We have grown from a printer with a single facility to a global marketing solutions provider with a seamless, integrated offering that creates more value for all our stakeholders at a time of significant media disruption. Together with LSC Communications, we will create a compelling combination of talent, expertise and client technology to further fuel our Quad 3.0 marketing solutions transformation and strengthen the role of print – a proven and trusted media form in today’s multichannel world.”

Quadracci isn't kidding when he calls it a defining moment for the company that was founded by his late father, Harry V. Quadracci, who left the W.A. Krueger Co. to found Quad/Graphics in 1971 by taking a $35,000 second mortgage on his home. Today, Quad/Graphics — a $4.2 billion company — employs 22,000 workers worldwide with 55 manufacturing and distribution facilities.

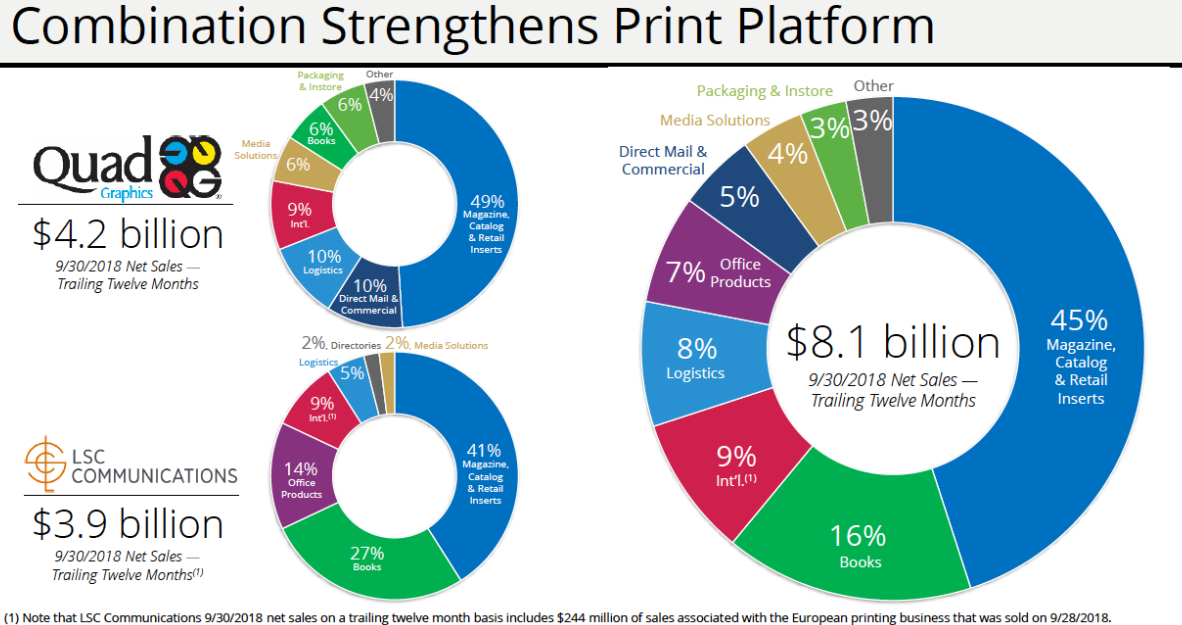

LSC Communications — an enterprise formed two years ago as part of a three-company spinoff of RR Donnelley (here's my take on what ultimately drove that 2016 spinoff) — is a $3.9 billion global company with 22,000 employees and 59 manufacturing and distribution facilities. Like Quad/Graphics, LSC derives a large portion of its revenues from the printing of magazines, catalogs and retail inserts. It also maintains a strong presence in the book manufacturing sector and will also provide Quad entrée into the office products business. Here is a chart that shows the breakdown of each company by market segments and what the combined printing business will look like:

The combined businesses will make Quad/Graphics an even more formidable printing industry powerhouse, especially when it comes to magazines and books. Click to enlarge.

Under the terms of the agreement, shareholders of the publicly-held LSC will receive 0.625 shares of Quad common stock for each LSC Communications share they own, representing a 34% premium based on LSC's pre-announcement stock price. Quad shareholders will continue to own Class A and Class B shares, representing approximately 71% total economic ownership and approximately 89% total voting power of the combined company. Within that, the Quadracci Family Voting Trust holds approximately 64% of the voting power of Quad’s outstanding common stock. Joel Quadracci will continue to lead the combined organization as chairman.

The future role of LSC Chairman Tom Quinlan following the deal completion was not mentioned in the press release or analyst/investor call.

Thomas J. Quinlan III, LSC Communications chairman, CEO and president, said: “Since becoming a standalone public company at the end of 2016, LSC Communications has added critical scale, capabilities and technologies. We have done so through acquisitions and divestitures as we work to strengthen our position as a leading innovator in print and multichannel logistics. We are now taking the next major step in our evolution." Quinlan wasn't kidding from the standpoint of LSC's aggressive M&A moves — but subsequent debt load — it has achieved in the past 24 months, easily making LSC the most active consolidator within the printing industry leading up to, what it appears, will be its own turn to be acquired.

Despite divesting its European footprint most recently, LSC Communications has mainly been a buyer, not a seller. In May 2018, it purchased RR Donnelley's Print Logistics business. That followed on the heels of its July 2017 acquisition of Fairrington Transportation, a mailing and logistics provider. LSC has become the industry leader when it comes to its co-mailing capabilities and transportation network.

In August of last year, LSC acquired Las Vegas-based Creel Printing for about $79 million, and the following month purchased publication printer Publishers Press, based in Lebanon Junction, Ky., for approximately $68 million. Both deals further bolstered its position in the publication printing sector. And, now with LSC's and Quad's proposed coupling, it will consolidate the consumer and B2B publication printing markets even further, which will give the combined organization considerably stronger pricing power.

Quad/Graphics was ranked No. 2 , and LSC Communications No. 3, on the most recent Printing Impressions 400 list of the largest printers in the U.S. and Canada, as ranked by annual sales. Their coupling will move them past RR Donnelley as the largest printer. (Click here to view the entire rankings in order to see where other leading printers fall on the list and which companies are their primary competitors within given market segments.)

In a conference call with investors and Wall Street analysts this morning, Quadracci, Quinlan and Dave Honan, executive VP and CFO at Quad/Graphics, were upbeat about the announcement, as expected. When questioned by an analyst about the $135 million in integration savings, Quadracci pointed to Quad's initiative to become an industry consolidator beginning in 2010, and its subsequent major acquisitions and integrations of World Color (2010), Vertis Communications (2013) and Brown Printing (2014), among other deals. In 2018, Quad further increased its 3.0 transformation into an integrated marketing solutions provider by acquiring Ivie and Rise Interactive.

"Quad has a proven track record of doing large-scale acquisitions," Quadracci said in response to the same analyst's questioning. "We're very process-driven." Adding that past acquisitions has required Quad to build a specialized integration team, he pointed to the process as being "very data-driven ... and we also use out heart as we make decisions." Quadracci also noted that moving customers to new plants following past acquisitions has resulted in a very high client retainment rate (in the high 90% range).

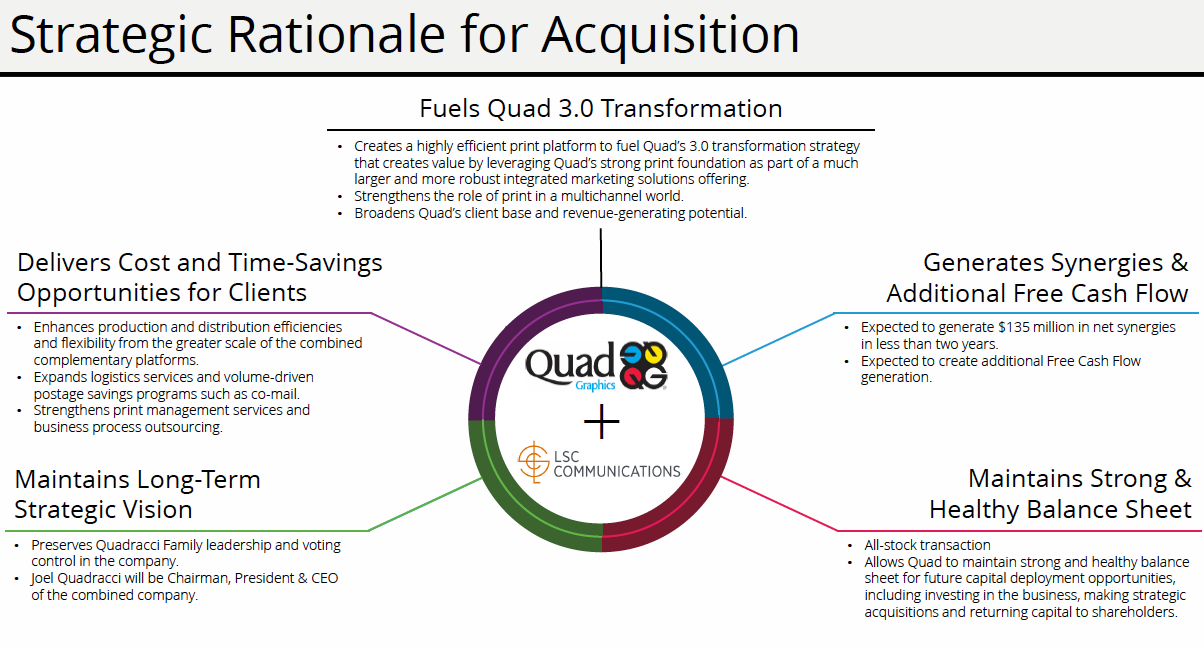

Quad and LSC senior executives held an investors call with Wall Street analysts to better explain the rationale of the acquisition. Click to enlarge.

Touting its projected dollar-for-dollar "cost to achieve" versus "annual net synergy" ratio, Honan indicated the $135 million savings of combining the two companies' operations will be achieved by $60 million in capacity rationalization, $50 million in administrative efficiencies and $25 million in supply chain management efficiencies.

Honan also projected that Quad's post-synergy pro forma debt leverage will be $1.905 billion and adjusted EBITDA will be $785 million, resulting in a 2.43x debt leverage ratio.

One question, surprisingly, that wasn't raised during the analyst call, from my perspective, was whether they fear the deal could be hampered by antitrust issues, due to the further consolidation that the transaction will pose for the catalog, book, and especially magazine, printing markets. Another unknown is how Wall Street will value the deal; RR Donnelley's split into three companies two years ago — with LSC as one of them — never did gain the valuations that they had anticipated.

And, unfortunately, the integration process and $135 million synergy savings goal of combining LSC into Quad will undoubtedly result in further printing plant consolidations and layoffs. Given that Quad/Graphics is the acquirer and that its production facilities, overall, are more automated in comparison to those operated by LSC, one might assume that LSC facilities will be the most in peril once the consolidation process begins.

Stay tuned. The aftershocks throughout the printing industry emanating from this week's announcement have just begun.

Mark Michelson now serves as Editor Emeritus of Printing Impressions. Named Editor-in-Chief in 1985, he is an award-winning journalist and member of several industry honor societies. Reader feedback is always encouraged. Email mmichelson@napco.com